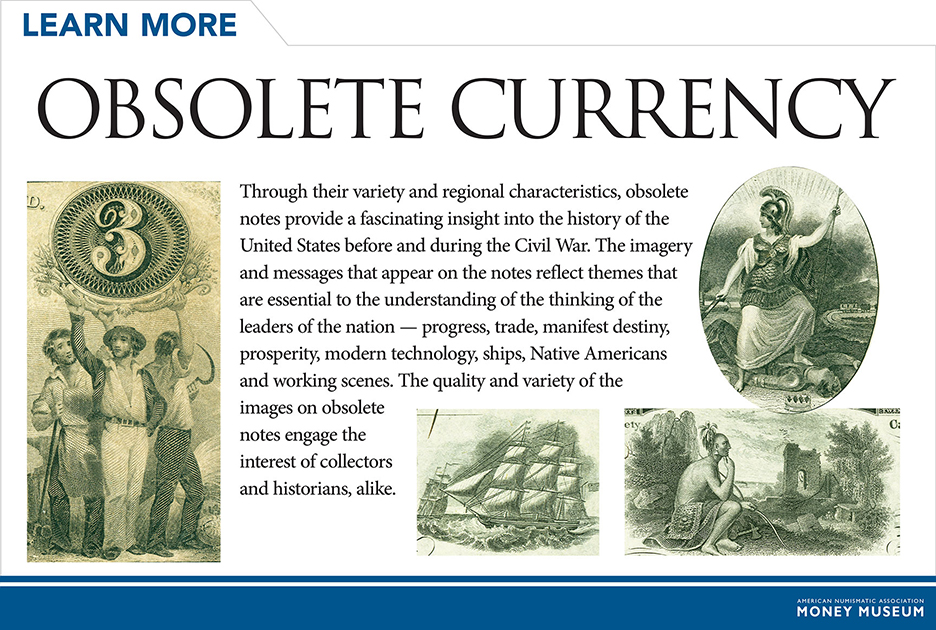

State-chartered banks and other private institutions provided the majority of currency known as obsolete notes that allowed the United States to grow from 1792 to 1866. This happened because the American government was unable to provide sufficient coinage to meet the nation’s economic needs. Since the Federal government refused to issue paper money, except in emergencies, and state governments were forbidden from doing so, banks and private institutions began producing their own paper currency to meet the needs of local commerce.

Over 8,000 institutions issued paper currency during the period, providing a substitute for coinage. Unfortunately obsolete notes had several drawbacks: They were only as reliable as the institution that issued them; the huge number and variety of note designs and issuers encouraged counterfeiting; and as a result, the notes were only accepted close to their place of origin — so that they could be cashed in for “real” money if need be. The Civil War brought an end to the era of obsolete notes as a result of the Federal government’s need to create a stable national currency to pay for the war.

Did You Know?

Obsolete banknotes come in a number of unusual denominations — including $1, $2, $3, $4, $5, $6, $7, $8 and $9 notes!

|

|

Click on the items in the case image below for an enhanced view